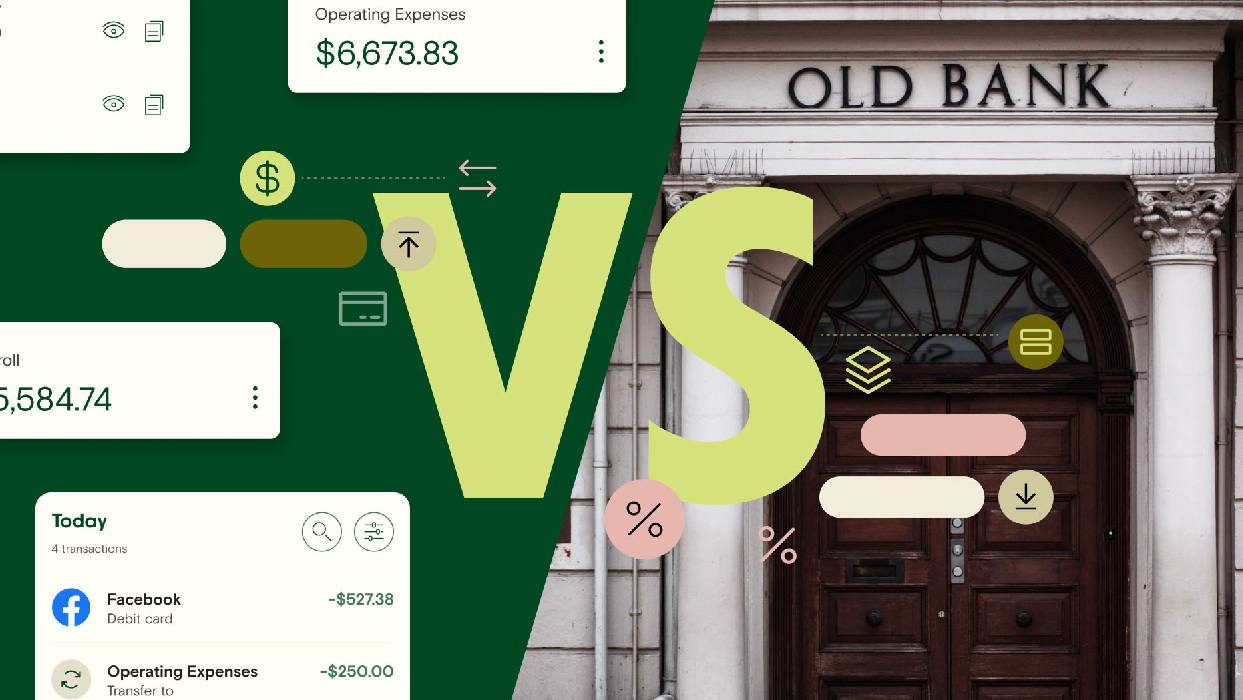

Part 1: The Emergence of Digital and Neo Banks

The financial landscape is undergoing a significant transformation, largely driven by the rise of digital and neo banks. These institutions are redefining traditional banking models by offering services that are not only more accessible but also cost-effective. Unlike conventional banks, digital banks operate exclusively online, eliminating the need for physical branches. This shift has been particularly appealing to younger, tech-savvy consumers who prioritize convenience and efficiency in their banking experiences. As these banks gain momentum, they are steadily capturing market share from established financial institutions.

Part 2: Key Features of Digital Banking

Digital banks have introduced innovative features that set them apart from traditional banks. Instant account opening is now available through intuitive mobile applications. Customers can track transactions in real-time. These apps also offer personalized financial insights. Additionally, lower fees and higher interest rates on savings accounts are often provided due to reduced operational costs. These advantages are made possible because operations are conducted entirely online, minimizing overhead expenses. Customers are increasingly drawn to these streamlined services, which cater to their fast-paced, digitally connected lifestyles.

Part 3: Why Young Consumers Prefer Neo Banks

Neo banks, a subset of digital banks, have gained immense popularity among younger generations. These institutions are specifically created to address the unique needs of millennials. They cater to Gen Z consumers who are highly adept at using technology. Neo banks offer seamless integration with financial management tools. They also integrate with budgeting apps and cryptocurrency services. Through these features, neo banks appeal to those seeking modern, flexible banking solutions. Furthermore, they focus on user experience and customer-centric design. This ensures that even complex financial tasks are simplified. It makes banking less intimidating for new users.

Part 4: Challenges Faced by Digital Banks

Despite their rapid growth, digital and neo banks face several challenges. Regulatory hurdles, cybersecurity threats, and limited access to credit products are some of the obstacles these institutions must navigate. Since they lack physical branches, building trust with customers who are accustomed to traditional banking can also be difficult. Additionally, while their cost-effective models are advantageous, they may struggle to compete. Large banks have extensive resources and established reputations. However, many digital banks are addressing these issues through strategic partnerships and continuous innovation.

Part 5: The Future of Banking: A Hybrid Approach?

As digital and neo banks continue to disrupt the industry, traditional banks are taking notice. Many are adopting aspects of the digital model by enhancing their online platforms and launching mobile-first initiatives. The future of banking may involve a hybrid approach. It could combine the reliability of traditional institutions with the agility of digital banks. For consumers, this means greater choice and improved services. Meanwhile, digital banks will likely keep pushing boundaries, further solidifying their role as key players in the evolving financial ecosystem.

Summary: The Digital Banking Revolution

Digital and neo banks are transforming the way people manage their finances by offering user-friendly, cost-efficient solutions. These institutions have gained significant traction, especially among younger, tech-savvy consumers who value convenience and innovation. While challenges like regulation and trust-building remain, their influence on the banking sector is undeniable. Traditional banks are responding by incorporating digital elements into their services, hinting at a future where both models coexist. As this revolution unfolds, consumers stand to benefit from enhanced banking experiences tailored to modern needs.

Leave a Reply